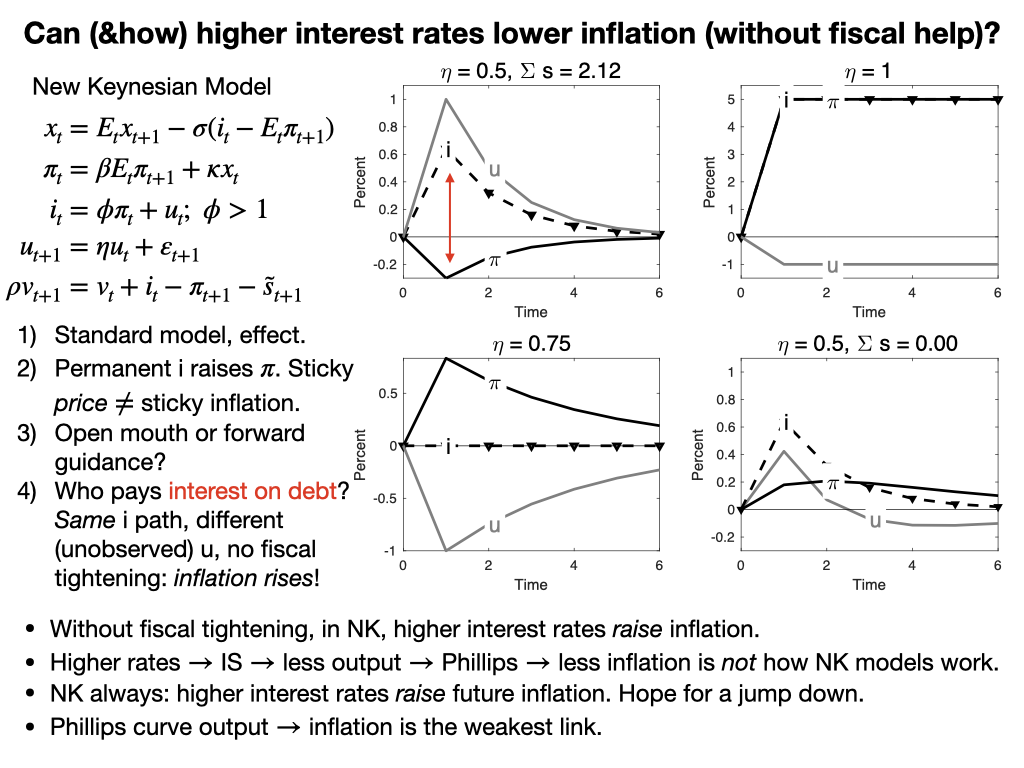

.

The equations are the utterly standard new-Keynesian model. The last equation tracks the evolution of the real value of the debt, which is usually in the footnotes of that model.

OK, top right, the standard result. There is a positive but temporary shock to the monetary policy rule, u. Interest rates go up and then slowly revert. Inflation goes down. Hooray. (Output also goes down, as the Phillips Curve insists.)

The next graph should give you pause on just how you interpreted the first one. What if the interest rate goes up persistently? Inflation rises, suddenly and completely matching the rise in interest rate! Yet prices are quite sticky -- k = 0.1 here. Here I drove the persistence all the way to 1, but that's not crucial. With any persistence above 0.75, higher interest rates give rise to higher inflation.

What's going on? Prices are sticky, but inflation is not sticky. In the Calvo model only a few firms can change price in any instant, but they change by a large amount, so the rate of inflation can jump up instantly just as it does. I think a lot of intuition wants inflation to be sticky, so that inflation can slowly pick up after a shock. That's how it seems to work in the world, but sticky prices do not deliver that result. Hence, the real interest rate doesn't change at all in response to this persistent rise in nominal interest rates. Now maybe inflation is sticky, costs apply to the derivative not the level, but absolutely none of the immense literature on price stickiness considers that possibility or how in the world it might be true, at least as far as I know. Let me know if I'm wrong. At a minimum, I hope I have started to undermine your faith that we all have easy textbook models in which higher interest rates reliably lower inflation.

(Yes, the shock is negative. Look at the Taylor rule. This happens a lot in these models, another reason you might worry. The shock can go in a different direction from observed interest rates.)

Panel 3 lowers the persistence of the shock to a cleverly chosen 0.75. Now (with sigma=1, kappa=0.1, phi= 1.2), inflation now moves with no change in interest rate at all. The Fed merely announces the shock and inflation jumps all on its own. I call this "equilibrium selection policy" or "open mouth policy." You can regard this as a feature or a bug. If you believe this model, the Fed can move inflation just by making speeches! You can regard this as powerful "forward guidance." Or you can regard it as nuts. In any case, if you thought that the Fed's mechanism for lowering inflation is to raise nominal interest rates, inflation is sticky, real rates rise, output falls and inflation falls, well here is another case in which the standard model says something else entirely.

Panel 4 is of course my main hobby horse these days. I tee up the question in Panel 1 with the red line. In that panel, the nominal interest are is higher than the expected inflation rate. The real interest rate is positive. The costs of servicing the debt have risen. That's a serious effect nowadays. With 100% debt/GDP each 1% higher real rate is 1% of GDP more deficit, $250 billion dollars per year. Somebody has to pay that sooner or later. This "monetary policy" comes with a fiscal tightening. You'll see that in the footnotes of good new-Keynesian models: lump sum taxes come along to pay higher interest costs on the debt.

Now imagine Jay Powell comes knocking to Congress in the middle of a knock-down drag-out fight over spending and the debt limit, and says "oh, we're going to raise rates 4 percentage points. We need you to raise taxes or cut spending by $1 trillion to pay those extra interest costs on the debt." A laugh might be the polite answer.

So, in the last graph, I ask, what happens if the Fed raises interest rates and fiscal policy refuses to raise taxes or cut spending? In the new-Keynesian model there is not a 1-1 mapping between the shock (u) process and interest rates. Many different u produce the same i. So, I ask the model, "choose a u process that produces exactly the same interest rate as in the top left panel, but needs no additional fiscal surpluses." Declines in interest costs of the debt (inflation above interest rates) and devaluation of debt by period 1 inflation must match rises in interest costs on the debt (inflation below interest rates). The bottom right panel gives the answer to this question.

Review: Same interest rate, no fiscal help? Inflation rises. In this very standard new-Keynesian model, higher interest rates without a concurrent fiscal tightening raise inflation, immediately and persistently.

Fans will know of the long-term debt extension that solves this problem, and I've plugged that solution before (see the "Expectations" paper above).

The point today: The statement that we have easy simple well understood textbook models, that capture the standard intuition -- higher nominal rates with sticky prices mean higher real rates, those lower output and lower inflation -- is simply not true. The standard model behaves very differently than you think it does. It's amazing how after 30 years of playing with these simple equations, verbal intuition and the equations remain so far apart.

The last two bullet points emphasize two other aspects of the intuition vs model separation. Notice that even in the top left graph, higher interest rates (and lower output) come with rising inflation. At best the higher rate causes a sudden jump down in inflation -- prices, not inflation, are sticky even in the top left graph -- but then inflation steadily rises. Not even in the top left graph do higher rates send future inflation lower than current inflation. Widespread intuition goes the other way.

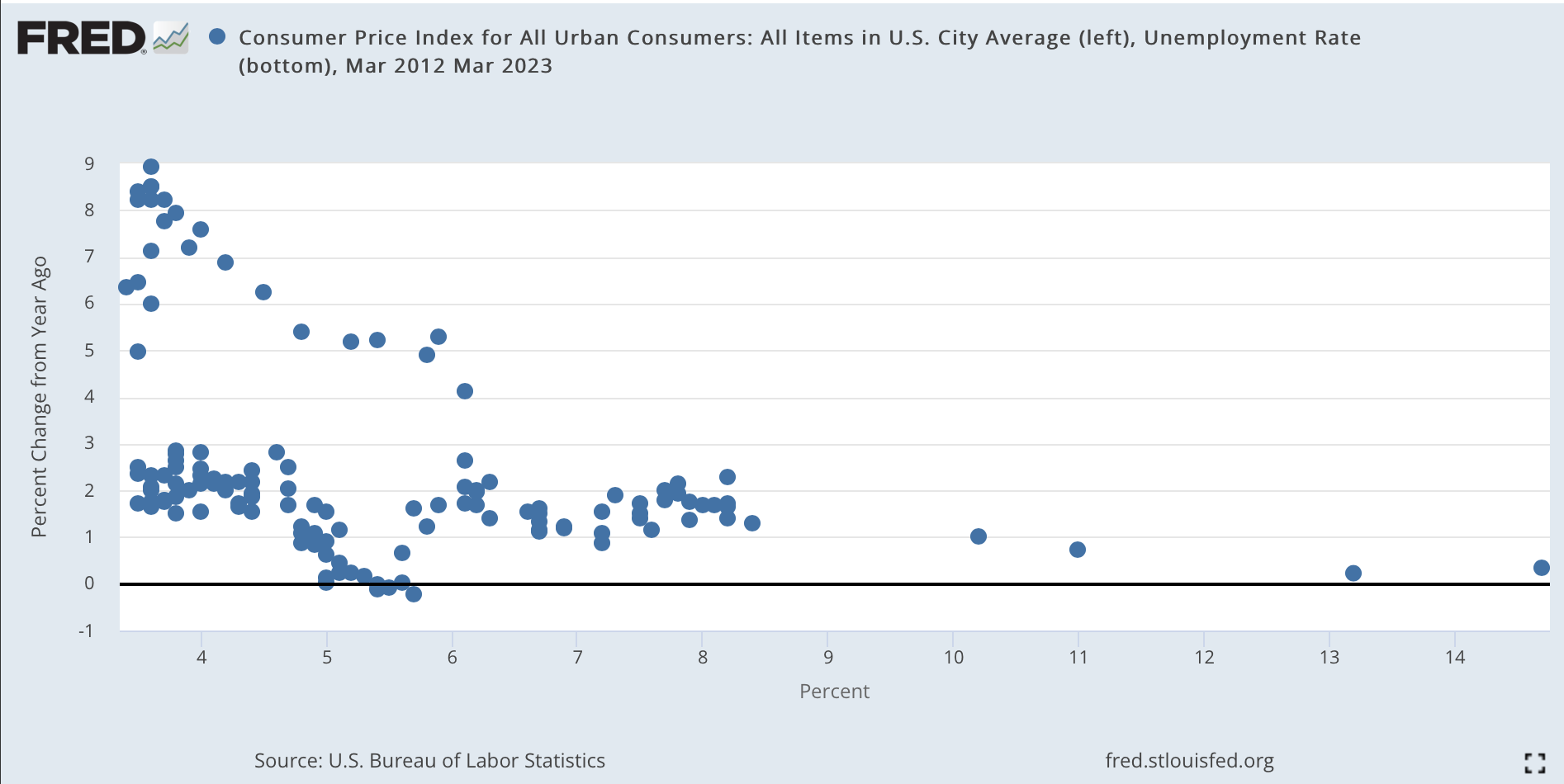

In all this theorizing, the Phillips Curve strikes me as the weak link. The Fed and common intuition make the Phillips Curve causal: higher rates cause lower output cause lower inflation. The original Phillips Curve was just a correlation, and Lucas 1972 thought of causality the other way: higher inflation fools people temporarily to producing more.

Here is the Phillips curve (unemployment x axis, inflation y axis) from 2012 through last month. The dots on the lower branch are the pre-covid curve, "flat" as common wisdom proclaimed. Inflation was still 2% with unemployment 3.5% on the eve of the pandemic. The upper branch is the more recent experience.

I think this plot makes some sense of the Fed's colossal failure to see inflation coming, or to perceive it once the dragon was inside the outer wall and breathing fire at the inner gate. If you believe in a Phillips Curve, causal from unemployment (or "labor market conditions") to inflation, and you last saw 3.5% unemployment with 2% inflation in February 2021, the 6% unemployment of March 2021 is going to make you totally ignore any inflation blips that come along. Surely, until we get well past 3.5% unemployment again, there's nothing to worry about. Well, that was wrong. The curve "shifted" if there is a curve at all.

But what to put in its place? Good question.

Update:

Lots of commenters and correspondents want other Phillips Curves. I've been influenced by a number of papers, especially "New Pricing Models, Same Old Phillips Curves?" by Adrien Auclert, Rodolfo Rigato, Matthew Rognlie, and Ludwig Straub, and "Price Rigidity: Microeconomic Evidence and Macroeconomic Implications" by Emi Nakamura and Jón Steinsson, that lots of different micro foundations all end up looking about the same. Both are great papers. Adding lags seems easy, but it's not that simple unless you overturn the forward looking eigenvalues of the system; "Expectations and the neutrality of interest rates" goes on in that way. Adding a lag without changing the system eigenvalue doesn't work.

Two more thoughts:

1) In the SBV debacle, many of my colleagues and friends jump to the conclusion, we should just mark all assets to market and forget about this "hold to maturity" business.

Not so fast. Like all imperfect patches, there is some logic to it. Suppose you have a $100 payment that you have to make in 10 years. To cover that payment, you buy a $100 face value Treasury zero coupon bond. Done, zero risk.

Now interest rates rise. The value of your asset has fallen in value! It's only worth, say, $90! Are you underwater? No, because when the time comes, you still will have exactly $100 to make the needed payment.

You will quickly answer, well, mark both assets and liabilities to market. The $100 payment is now also worth $90, so marking both sides to market would reveal no change. But there is a lot of unneeded volatility here. And in most cases, the $100 payment is not tradeable on a market, while the $100 asset is. So now, you're going to be balancing marking to market vs. marking to model. Add the regulator's and many participant's distrust of market prices, which are always seemingly "illiquid," "distressed," in a state of "fire sale," "dysfunctional," and so forth. Add the pointlessness of it all. In this situation we all know that you can make the payment in 10 years. Lock it up and ignore it. Call the asset "hold to maturity."

Of course, suppose the point of that asset is to make sure that depositors with $100 accounts can always get their money back by selling the asset. Well, now we have Silicon Valley Bank.

Hence the imperfect fudge of current accounting and regulation rules. "Hold to maturity" assets don't get marked to market, and indeed there are penalties for selling them to meet current needs. Lots of "liquidity" and other rules are supposed to make sure there are adequate short run liabilities to stop a run. Those were of course completely absent in SBV's case -- a truly spectacular failure of elementary regulation.

In short, mark to market makes sense to assess if a bank can make its payments and avoid failure tomorrow. Hold to maturity makes a bit of sense to assess if a bank can make its payments and avoid failure years from now, when both long term assets and long term liabilities come due. That is, if it survives that long.

2) There is a lot of criticism of SBV bank management and board for being underinvested in risk management and over invested in lobbying, political connections, donations to politically popular causes, and so forth. Ex post, their choice of managerial investments looks brilliant! What brought in the millions to stem a run, I ask you? In today's highly political banking system, they made optimal choices. To an economist, many puzzling actions are just an optimal answer to a different question.

Update: Ok, I went too far with that one. Management are out, shareholders wiped out. I'll stick with the idea that uninsured depositors did a great job of monitoring -- they monitored that the bank had the political chops to demand and get a bailout of uninsured depositors!

From a correspondent:

"It seems to me now that SVB was really a money market fund with the addition of a bit of equity and breaking all the SEC asset and liquidity rules that MMFs are subject to. "

Or, it was really a mutual fund (money market funds with $1 values can't invest in long term bonds, long term bond funds must have floating NAV) that was violating rules on floating NAV!

Three small thoughts.

1) There is much commentary that bank troubles will interfere with the Fed's plan to lower inflation by raising rates. Actually, this is a feature not a bug. The main mechanism by which, in the Fed's view, raising interest rates slows the economy and lowers inflation is by "constricting credit," "tightening financial conditions," lowering borrowing that finances investment and consumer durables purchases. The Fed didn't want runs, no, but it wants the result. If you don't like that, well, we need to think of other ways to contain inflation, like taking the fiscal gasoline off the fire.

2) On uninsured deposits. A correspondent suggests that the Fed simply mandate that all large depositors participate in the sorts of services, there for the asking, that split large accounts into multiple $249k accounts spread over multiple banks, or sweeps into money market funds.

I don't think that mandating this system is a good idea. If you're going to do that, of course, you might as well just insure all deposits and keep it simple.

But the suggestion prompts doubt over the oft repeated notion that we want large sophisticated depositors to monitor banks. Anyone who was large and sophisticated enough to monitor banks had already gamed the system to make sure their accounts were insured, at some nontrivial cost in fees and trouble. The only people left with millions in checking accounts were, sort of by definition, financially unsophisticated or too busy running actual companies to bother with this sort of thing. Sort of like taxes.

We might as well give in, that all deposits are here forth insured. If so, of course, then banks are totally gambling with the house's money. But we also have to give in that if they can't spot this elephant in the room, asset risk regulation is hopeless. The only workable answer (of course) is narrow deposit taking -- all runnable deposits invested in reserves and short term treasuries; fund portfolios of long term debt with long-term borrowing (CDs for example) and lots of equity.

3) Liquidity and fixed value are no longer necessarily tied together. I still don't quite get why better payment services are not attached to floating value funds. Then we wouldn't need run-prone bank accounts at all.

With amazing speed and impeccable timing, Erica Jiang, Gregor Matvos, Tomasz Piskorski, and Amit Seru analyze how exposed the rest of the banking system is to an interest rate rise.

Recap: SVB failed, basically, because it funded a portfolio of long-term bonds and loans with run-prone uninsured deposits. Interest rates rose, the market value of the assets fell below the value of the deposits. When people wanted their money back, the bank would have to sell at low prices, and there would not be enough for everyone. Depositors ran to be the first to get their money out. In my previous post, I expressed astonishment that the immense bank regulatory apparatus did not notice this huge and elementary risk. It takes putting 2+2 together: lots of uninsured deposits, big interest rate risk exposure. But 2+2=4 is not advanced math.

How widespread is this issue? And how widespread is the regulatory failure? One would think, as you put on the parachute before jumping out of a plane, that the Fed would have checked that raising interest rates to combat inflation would not tank lots of banks.

Banks are allowed to report the "hold to maturity" "book value" or face value of long term assets. If a bank bought a bond for $100 (book value) or if a bond promises $100 in 10 years (hold to maturity value), basically, the bank may say it's worth $100, even though the bank might only be able to sell the bond for $75 if they need to stop a run. So one way to put the issue is, how much lower are mark to market values than book values?

The paper (abstract):

The U.S. banking system’s market value of assets is $2 trillion lower than suggested by their book value of assets accounting for loan portfolios held to maturity. Marked-to-market bank assets have declined by an average of 10% across all the banks, with the bottom 5th percentile experiencing a decline of 20%.

... 10 percent of banks have larger unrecognized losses than those at SVB. Nor was SVB the worst capitalized bank, with 10 percent of banks have lower capitalization than SVB. On the other hand, SVB had a disproportional share of uninsured funding: only 1 percent of banks had higher uninsured leverage.

... Even if only half of uninsured depositors decide to withdraw, almost 190 banks are at a potential risk of impairment to insured depositors, with potentially $300 billion of insured deposits at risk. ... these calculations suggests that recent declines in bank asset values very significantly increased the fragility of the US banking system to uninsured depositor runs.

Data:

we use bank call report data capturing asset and liability composition of all US banks (over 4800 institutions) combined with market-level prices of long-duration assets.

How big and widespread are unrecognized losses?

The average banks’ unrealized losses are around 10% after marking to market. The 5% of banks with worst unrealized losses experience asset declines of about 20%. We note that these losses amount to a stunning 96% of the pre-tightening aggregate bank capitalization.

|

| Percentage of asset value decline when assets are mark-to- market according to market price growth from 2022Q1 to 2023Q1 |

The median bank funds 9% of their assets with equity, 65% with insured deposits, and 26% with uninsured debt comprising uninsured deposits and other debt funding....SVB did stand out from other banks in its distribution of uninsured leverage, the ratio of uninsured debt to assets...SVB was in the 1st percentile of distribution in insured leverage. Over 78 percent of its assets was funded by uninsured deposits.

But it is not totally alone

the 95th percentile [most dangerous] bank uses 52 percent of uninsured debt. For this bank, even if only half of uninsured depositors panic, this leads to a withdrawal of one quarter of total marked to market value of the bank.

|

| Uninsured deposit to asset ratios calculated based on 2022Q1 balance sheets and mark-to-market values |

Overall, though,

...we consider whether the assets in the U.S. banking system are large enough to cover all uninsured deposits. Intuitively, this situation would arise if all uninsured deposits were to run, and the FDIC did not close the bank prior to the run ending. ...virtually all banks (barring two) have enough assets to cover their uninsured deposit obligations. ... there is little reason for uninsured depositors to run.

... SVB, is [was] one of the worst banks in this regard. Its marked-to-market assets are [were] barely enough to cover its uninsured deposits.

Breathe a temporary sigh of relief.

I am struck in the tables by the absence of wholesale funding. Banks used to get a lot of their money from repurchase agreements, commercial paper, and other uninsured and run-prone sources of funding. If that's over, so much the better. But I may be misunderstanding the tables.

Summary: Banks were borrowing short and lending long, and not hedging their interest rate risk. As interest rates rise, bank asset values will fall. That has all sorts of ramifications. But for the moment, there is not a danger of a massive run. And the blanket guarantee on all deposits rules that out anyway.

Their bottom line:

There are several medium-run regulatory responses one can consider to an uninsured deposit crisis. One is to expand even more complex banking regulation on how banks account for mark to market losses. However, such rules and regulation, implemented by myriad of regulators with overlapping jurisdictions might not address the core issue at hand consistently

I love understated prose.

There does need to be retrospective. How are 100,000 pages of rules not enough to spot plain-vanilla duration risk -- no complex derivatives here -- combined with uninsured deposits? If four authors can do this in a weekend, how does the whole Fed and state regulators miss this in a year? (Ok, four really smart and hardworking authors, but still... )

Alternatively, banks could face stricter capital requirement... Discussions of this nature remind us of the heated debate that occurredafter the 2007 financial crisis, which many might argue did not result in sufficient progress on bank capital requirements...

My bottom line (again)

This debacle goes to prove that the whole architecture is hopeless: guarantee depositors and other creditors, regulators will make sure that banks don't take too many risks. If they can't see this, patching the ship again will not work.

If banks channeled all deposits into interest-paying reserves or short-term treasury debt, and financed all long-term lending with long-term liabilities, maturity-matched long-term debt and lots of equity, we would end private sector financial crises forever. Are the benefits of the current system worth it? (Plug for "towards a run-free financial system." "Private sector" because a sovereign debt crisis is something else entirely.)

(A few other issues stand out in the SVB debacle. Apparently SVB did try to issue equity, but the run broke out before they could do so. Apparently, the Fed tried to find a buyer, but the anti-merger sentiments of the administration plus bad memories of how buyers were treated after 2008 stopped that. Beating up on mergers and buyers of bad banks has come back to haunt our regulators.)

Update:

(Thanks to Jonathan Parker) It looks like the methodology does not mark to market derivatives positions. (It would be hard to see how it could do so!) Thus a bank that protects itself with swap contracts would look worse than it actually is. (Translation: Banks can enter a contract that costs nothing, in which they pay a fixed rate of interest and receive a floating rate of interest. When interest rates go up, this contract makes a lot of money! )

Amit confirms,

As we say in our note, due to data limitations, we do not account for interest rate hedges across the banks. As far as we know SVB was not using such hedges...

Of course if they are, one has to ask who is the counterparty to such hedges and be sure they won't similarly blow up. AIG comes to mind.

He adds:

note we don’t account for changes in credit risk on the asset side. All things equal this can make things worse for borrowers and their creditors with increases in interest rates. Think for a moment about real estate borrowers and pressures in sectors such as commercial real estate/offices etc. One could argue this number would be large.

So don't sleep too well.

From an email correspondent:

Besides regulation, accountancy itself is a joke. KPMG Gave SVB, Signature Bank Clean Bill of Health Weeks Before Collapse.

How can unrealised losses near equal to a bank's capital be ignored in the true and fair assessment of its financial condition (the core statement of an audit leaving out all the disclaimers) just because it was classified as Held to Maturity owing some nebulous past "intention" (whatever that was ever worth) not to sell?

It strikes me that both accounting and regulation have become so complicated that they blind intelligent people to obvious elephants in the room.

The Silicon Valley Bank failure strikes me as a colossal failure of bank regulation, and instructive on how rotten the whole edifice is. I write this post in an inquisitive spirit. I don't know the details of how SVB was regulated, and I hope some readers do and can chime in.

As reported so far by media, the collapse was breathtakingly simple. SVB paid a bit higher interest rates than the measly 0.01% (yes) that Chase offers. It attracted large deposits from venture capital backed firms in the valley. Crucially, only the first $250,000 are insured, so most of those deposits are uninsured. The deposits are financially savvy customers who know they have to get in line first should anything go wrong. SVB put much of that money into long-maturity bonds, hoping to reap the difference between slightly higher long-term interest rates and what it pays on deposits. But as we've known for hundreds of years, if interest rates rise, then the market value of those long-term bonds fall. Now if everyone comes asking for their money back, the assets are not worth enough to pay everyone back.

In sum, you have "duration mismatch" plus run-prone uninsured depositors. We teach this in the first week of an MBA or undergraduate banking class. This isn't crypto or derivatives or special purpose vehicles or anything fancy.

Where were the regulators? The Dodd Frank act added hundreds of thousands of pages of regulations, and an army of hundreds of regulators. The Fed enacts "stress tests" in case regular regulation fails. How can this massive architecture fail to spot basic duration mismatch and a massive run-prone deposit base? It's not hard to fix, either. Banks can quickly enter swap contracts to cheaply alter their exposure to interest rate risk without selling the whole asset portfolio.

Michael Cembalist assembled numbers. This wasn't hard to see.

Even Q3 2022 -- a long time ago -- SVB was a huge outlier in having next to no retail deposits (vertical axis, "sticky" because they are insured and regular people), and a huge asset base of loans and securities.

Michael then asks

.. how much duration risk did each bank take in its investment portfolio during the deposit surge, and how much was invested at the lows in Treasury and Agency yields? As a proxy for these questions now that rates have risen, we can examine the impact on Common Equity Tier 1 Capital ratios from an assumed immediate realization of unrealized securities losses ... That’s what is shown in the first chart: again, SVB was in a duration world of its own as of the end of 2022, which is remarkable given its funding profile shown earlier.

Again, in simpler terms. "Capital" is the value of assets (loans, securities) less debt (mostly deposits). But banks are allowed to put long-term assets into a "hold to maturity" bucket, and not count declines in the market value of those assets. That's great, unless people knock on the door and ask for their money now, in which case the bank has to sell the securities, and then it realizes the market value. Michael simply asked how much each bank was worth in Q42002 if it actually had to sell its assets. A bit less in each case -- except SVB (third from left) where the answer is essentially zero. And Michael just used public data. This is not a hard calculation for the Fed's team of dozens of regulators assigned to each large bank.

Perhaps the rules are at fault? If a regulator allows "hold to maturity" accounting, then, as above, they might think the bank is fine. But are regulators really so blind? Are the hundreds of thousands of pages of rules stopping them from making basic duration calculations that you can do in an afternoon? If so, a bonfire is in order.

This isn't the first time. Notice that when SBF was pillaging FTX customer funds for proprietary trading, the SEC did not say "we knew all about this but didn't have enough rules to stop it." The Bank of England just missed a collapse of pension funds who were doing exactly the same thing: borrowing against their long bonds to double up, and forgetting that occasionally markets go the wrong way and you have to sell to make margin calls. (That's week 2 of the MBA class.)

Ben Eisen and Andrew Ackerman in WSJ ask the right question (10 minutes before I started writing this post!) Where Were the Regulators as SVB Crashed?

“The aftermath of these two cases is evidence of a significant supervisory problem,” said Karen Petrou, managing partner of Federal Financial Analytics, a regulatory advisory firm for the banking industry. “That’s why we have fleets of bank examiners, and that’s what they’re supposed to be doing.”

The Federal Reserve was the primary federal regulator for both banks.

Notably, the risks at the two firms were lurking in plain sight. A rapid rise in assets and deposits was recorded on their balance sheets, and mounting losses on bond holdings were evident in notes to their financial statements.

moreover,

“Rapid growth should always be at least a yellow flag for supervisors,” said Daniel Tarullo, a former Federal Reserve governor who was the central bank’s point person on regulation following the financial crisis...

In addition, nearly 90% of SVB’s deposits were uninsured, making them more prone to flight in times of trouble since the Federal Deposit Insurance Corp. doesn’t stand behind them.

90% is a big number. Hard to miss. The article echoes some confusion about "liquidity"

SVB and Silvergate both had less onerous liquidity rules than the biggest banks. In the wake of the failures, regulators may take a fresh look at liquidity rules,...

This is absolutely not about liquidity. SBV would have been underwater if it sold all its securities at the bid prices. Also

Silvergate and SVB may have been particularly susceptible to the change in economic conditions because they concentrated their businesses in boom-bust sectors...

That suggests the need for regulators to take a broader view of the risks in the financial system. “All the financial regulators need to start taking charge and thinking through the structural consequences of what’s happening right now,” she [Saule Omarova] said

Absolutely not! I think the problem may be that regulators are taking "big views," like climate stress tests. This is basic Finance 101 measure duration risk and hot money deposits. This needs a narrow view!

There is a larger implication. The Fed faces many headwinds in its interest rate raising effort. For example, each point of higher real interest rates raises interest costs on the debt by about $250 billion (1 percent x 100% debt/GDP ratio). A rate rise that leads to recession will lead to more stimulus and bailout, which is what fed inflation in the first place.

But now we have another. If the Fed has allowed duration risk to seep in to the too-big to fail banking system, then interest rate rises will induce the hard choice between yet more bailout and a financial storm. Let us hope the problem is more limited - as Michael's graphs suggest.

Why did SVB do it? How could they be so blind to the idea that interest rates might rise? Why did Silicon Valley startups risk cash, that they now claim will force them to bankruptcy, in uninsured deposits? Well, they're already clamoring for a bailout. And given 2020, in which the Fed bailed out even money market funds, the idea that surely a bailout will rescue us should anything go wrong might have had something to do with it.

(On the startup bailout. It is claimed that the startups who put all their cash in SVB will now be forced to close, so get going with the bailout now. It is not startups who lose money, it is their venture capital investors, and it is they who benefit from the bailout.

Let us presume they don't suffer sunk cost fallacy. You have a great company, worth investing $10 million. The company loses $5 million of your cash before they had a chance to spend it. That loss obviously has nothing to do with the company's prospects. What do you do? Obviously, pony up another $5 million and get it going again. And tell them to put their cash in a real bank this time.)

How could this enormous regulatory architecture miss something so simple?

This is something we should be asking more generally. 8% inflation. Apparently simple bank failures. What went wrong? Everyone I know at the Fed are smart, hard working, honest and dedicated public servants. It's about the least political agency in Washington. Yet how can we be seeing such simple o-ring level failures?

I can only conclude that this overall architecture -- allow large leverage, assume regulators will spot risks -- is inherently broken. If such good people are working in a system that cannot spot something so simple, the project is hopeless. After all, a portfolio of long-term treasuries is about the safest thing on the planet -- unless it is financed by hot money deposits. Why do we have teams of regulators looking over the safest assets on the planet? And failing? Time to start over, as I argued in Towards a run free financial system

Or... back to my first question, am I missing something?

****

Updates:

A nice explainer thread (HT marginal revolution). VC invests in a new company. SVB offers an additional few million in debt, with one catch, the company must use SVB as the bank for deposits. SVB invests the deposits in long-term mortgage backed securities. SVB basically prints up money to use for its investment!

"SVB goes to founders right after they raise a very, very expensive venture round from top venture firms offering:

- 10-30% of the round in debt

- 12-24 month term

- interest only with a balloon payment

- at a rate just above prime

For investors, it also seems like a no-downside scenario for your portfolio: Give up 10-25 bps in dilution for a gigantic credit facility at functionally zero interest rate.

If your PortCo doesn't need it, the cash just sits. If they do, it might save them in a crunch. The deals typically have deposit covenants attached. Meaning: you borrow from us, you bank with us.

And everyone is broadly okay with that deal. It's a pretty easy sell! "You need somewhere to put your money. Why not put it with us and get cheap capital too?"

Update:

1) Old Eagle Eye's comment below is fascinating. I am getting the sense that the rules actually preclude putting 2+2=4 together here. Copied here in toto

SIVB did have a hedge put on during 2022, but it was limited to its available-for-sale securities ("AFS"). It was precluded from hedging its interest rate risk in held-to-maturity securities ("HTM") by U.S. GAAP rules. [My emphasis] Here is the explanation found at PwC:

[PWC Viewpoint Commentary: "The notion of hedging the interest rate risk in a security classified as held to maturity is inconsistent with the held-to-maturity classification under ASC 320, which requires the reporting entity to hold the security until maturity regardless of changes in market interest rates. For this reason, ASC 815-20-25-43(c)(2) indicates that interest rate risk may not be the hedged risk in a fair value hedge of held-to-maturity debt securities." "ASC 815-20-25-12(d) provides guidance on the eligibility of held-to-maturity debt securities for designation as a hedged item in a fair value hedge."]

[Extracted subsection:

"Chapter 6: Hedges of financial assets and liabilities.

"6.4 Hedging fixed-rate instruments

"6.4.3.4 Hedging held-to-maturity debt securities

"ASC 815-20-25-12(d)

"If the hedged item is all or a portion of a debt security (or a portfolio of similar debt securities) that is classified as held to maturity in accordance with Topic 320, the designated risk being hedged is the risk of changes in its fair value attributable to credit risk, foreign exchange risk, or both. If the hedged item is an option component of a held-to-maturity security that permits its prepayment, the designated risk being hedged is the risk of changes in the entire fair value of that option component. If the hedged item is other than an option component of a held-to-maturity security that permits its prepayment, the designated hedged risk also shall not be the risk of changes in its overall fair value."]

Source: PWC Viewpoint (viewpoint.pwc.com) Publication date: 31 Jul 2022

https://viewpoint.pwc.com/dt/us/en/pwc/accounting_guides/derivatives_and_hedg/derivatives_and_hedg_US/chapter_6_hedges_of__US/64_hedging_fixedrate_US.html

Home Bias in Economics Journals is an interesting new paper by Dirk Bethmann, Felix Bransch, Michael Kvasnicka, and Abdolkarim Sadrieh (via Marginal Revolution).

...Researchers from Harvard, but also nearby Massachusetts Institute of Technology (MIT), and from Chicago (co-)author a disproportionate share of articles in their respective home journal.... We study this question in a difference-in-differences framework, using data on both current and past author affiliations and cumulative citation counts for articles published between 1995 and 2015 in the QJE, JPE, and American Economic Review (AER), which serves as a benchmark. We find that median article quality is lower in the QJE if authors have ties to Harvard and/or MIT than if authors are from other top-10 universities, but higher in the JPE if authors have ties to Chicago. We also find that home ties matter for the odds of journals to publish highly influential and low impact papers. Again, the JPE appears to benefit, if anything, from its home ties, while the QJE does not.

On the bottom end as well,

articles with a Chicago aliation in the JPE are less likely to be amongst the group of relatively low impact articles (i.e., to rank among the 25% or 10% of least cited articles published in the three journals in a year) than articles in the JPE authored by researchers from other top-10 institutions.

Those are the what, but not the why. These findings naturally provoke some thought from my time at Chicago, and as JPE editor.

While I was at the JPE there was an explicit ethic about these matters. Yes, the JPE publishes papers by Chicago faculty, but only the best ones. Faculty were expected to self-select the best papers, especially innovative ones that have trouble elsewhere, but are likely to have impact t. That ethic was even stronger for Chicago PhD dissertations. The JPE really really discouraged Chicago Ph.D. dissertations, and only very rarely published them. (I'm curious how much of the JPE/QJE difference comes down to dissertations rather than faculty papers).

When I was there, there were only four editors, all based at Chicago. There was also a rule that a second editor had to sign off on any revision and on any publication decision. This was wonderful discipline, and I learned a lot from my fellow editors' view of papers. That procedure also helps to enforce the higher bar standard. All being from the same institution helped a well to produce collegiality, as well as interest in keeping up the brand.

Some of my hardest times as editor came from rejecting colleagues' pretty good but not good enough papers. For colleagues, I also was strict about the one revision rule, and rejecting a few promising but still not ready papers from colleagues (and friends) caused more heartache.

The JPE also had a culture of decisive editing. The referees provide advice, but the editor makes decisions. This culture leads to publishing the kind of innovative papers that referees may disparage, especially when an author crosses field boundaries and invades sensitive turf.

In this way a home journal, run by a small number of long-term editors, with an institutional reputation, is different than an association journal, with a large board of coeditors who serve short times, and act independently.

I benefited from the JPE's policies. Sherwin Rosen published "Time consistent health insurance" over referee objections, though of course asking for a revision that addressed those objections. "The Random Walk in GNP," my first big paper, was published in the JPE after being rejected elsewhere. "Determinacy and Identification," a sprawling new-Keynesian critique, could never have been published anywhere else. "A simple test of consumption insurance" (as well as Barb Mace's "Full Insurance" which inspired my paper, a worthy exception to the rule against PhD theses) would likely have had a terrible time anywhere else. John Campbell and I might have published By Force of Habit elsewhere, but the JPE editor was important to boiling it down and focusing it.

Was it a good idea for the JPE to publish these, or would the world be better if half had spent another few years batting from journal to journal, and half ended up not published at all? Of course, perhaps there were other, better, papers from outsiders that the JPE could have published. You judge.

I also have plenty of papers rejected by the JPE, even desk rejected. And most of my papers get rejected by at least 3 or 4 journals before finding a home. Welcome to the club.

Things have changed. The JPE is a much bigger journal, with a big and spread out editorial board. Other journals, like the AER, have also expanded and added sub journals. Perhaps the concept of a small general interest journal, run by decisive editors willing to take some risk in the quest of innovative papers, publishing papers that at least two of four editors can understand and judge, is out of date; nostalgia for a simpler time. I hope the new JPE retains the special character that made the old JPE so good.

From the Wall Street Journal Feb 2. After 30 days I can post full text.

A Consumption Tax Is the Shock Our Broken System Needs

Something remarkable happened last month. On Jan. 9, Georgia Rep. Buddy Carter introduced the “Fair Tax” bill to the House of Representatives, and secured a promise of a floor vote. The bill eliminates the personal and corporate income tax, estate and gift tax, payroll (Social Security and Medicare) tax and the Internal Revenue Service. It replaces them with a single national sales tax. Business investment is exempt, so it is effectively a consumption tax. Each household would get a check each month, so that purchases up to the poverty line are effectively not taxed.

Mainstream media and Democrats instantly deplored the measure. Mother Jones said it would “turbocharge inequality.” Rep. Pramila Jayapal called it a “tax cut for the rich, period.” The New Republic asserted that consumption taxes are “always a dumb idea”—but presumably not in Europe, where 20% value-added taxes finance welfare states—and called it a “Republican dream to build a wealth aristocracy.”

Even the Journal’s editorial board disapproved, though mostly on politics rather than substance, admitting a consumption tax “might make sense” if Congress were “writing the tax code from scratch.” The board worried that we might end up with income and sales taxes, like Europe. And the tax change won’t pass, making it is a “masochistic vote” that it will “give Democrats a potent campaign issue.”

But our income and estate tax system is broken. It has high statutory rates with a Swiss cheese of exemptions, immense cost, unfairness and distortion. Former President Trump’s taxes are Exhibit A, no longer making headlines because we learned that he simply aggressively exploits the complex rules and deductions that Congress offers to wealthy politically connected real-estate investors.

A consumption tax, with none of the absurd complexity of our current taxes, is the answer. It funds the government with the least economic distortion. A consumption tax need not be regressive. It’s easy enough to exempt the first few thousand dollars of consumption, or add to the rebate.

More important, the progressivity of a whole tax and transfer system matters, not of a particular tax in isolation. If a flat consumption tax finances greater benefits to people of lesser means, the overall system could be more progressive than what we have now. A consumption tax would still finance food stamps, housing, Medicaid, and so forth. And it would be particularly efficient at raising revenue, meaning there would potentially be more to distribute—a point that has led some conservatives to object to a consumption tax.

Others complain that the rate will be high. An effective 30% consumption tax, added to state sales taxes as high as 10%, could add up to a 40% or greater rate. But taxes overall must finance what the government spends. Collecting it in one tax rather than lots of smaller taxes doesn’t change the overall rate. It’s better for voters to see how much the government takes.

A range of implicit subsidies will disappear. Good. Subsidies should be transparent. Money for electric cars, health insurance, housing, and so forth should be appropriated and sent as checks, not hidden as tax deductions or credits. They can still be as large as Congress and voters wish. However, it is vital to keep the tax at a flat rate and not try to redistribute income or subsidize industries by different tax rates.

Will there be some problems of compliance and evasion? Probably, but sales taxes or value-added taxes are hardly new, untested ideas. The Fair Tax bill addresses many objections and real-world concerns, and more refinements can follow. A value-added tax or personal-consumption tax can achieve similar goals.

This is a big moment. For a long time, consumption taxes have been debated in academic articles, books, think-tank reports, administration white papers and so forth. When the U.S. eventually decides to reform the tax code, consumption taxes will be the obvious answer. It is great news that real elected politicians like Rep. Carter get it, and are willing to stick their necks out to try to get it passed.

No, it’s not likely to pass this year, or next. All great reforms take time. The 8-hour workday and Social Security started as wild-eyed dreams of the socialist party. Civil rights took bill after bill being voted down. The income tax took a long time. But if we never talk about the promised land and only squabble over the next fork in the road, surely we will never get there.

At the AEI fiscal theory event last Tuesday Tom Sargent and Eric Leeper made some key points about the current situation, with reference to lessons of history.

Tom's comments updated his excellent paper with George Hall "Three World Wars" (at pnas, summary essay in the Hoover Conference volume). Tom and George liken covid to a war: a large emergency requiring immense expenditure. We can quibble about "require" but not the expenditure.

(2008 was a little war in this sense as well.) Since outlays are well ahead of receipts, these huge temporary expenditures are financed by issuing debt and printing money, as optimal tax theory says they should be.

In all three cases, you see a ratcheting up of outlays after the war. That's happening now, and in 2008, just as in WWI and WWII.

After WWI and WWII, there is a period of primary surpluses -- tax receipts greater than spending -- which helps to pay back the debt. This time is notable for the absence of that effect.

We see that most clearly by plotting the primary deficits directly. The data update since Tom and George's original paper (dots) makes that clear. To a fiscal theorist, this is a worrisome difference. We are not following historical tradition of regular, full employment, peacetime surpluses.

The two world wars were also financed by a considerable inflation. The important consequence of inflation is that it inflates away government debt. Essentially, we pay for part of the war by a default on debt, engineered via inflation.

1947 is an interesting case. As now, inflation broke out, the Fed left interest rates alone, and the inflation went away once it had inflated away enough debt. That too is an interesting episode in the debate whether the Fed must move rates more than one for one to keep inflation from spiraling away.

The effect of inflation is clearer in the next graph, which plots the real return on government bonds:

Two great videos just dropped related to fiscal theory.

The first is an "Uncommon Knowledge" interview with Peter Robinson. We start with fiscal theory and move on far and wide. Peter is a great interviewer, and the Uncommon Knowledge production team put together a great video of it. Pick your link: Video at Hoover (best, in my view); Hoover event page with podcast, links and more info, Youtube, Twitter, Facebook.

Second, Michael Strain at AEI moderated a great panel discussion on fiscal theory with me, Robert Barro, Tom Sargent and Eric Leeper. Three of the founding fathers of fiscal theory offer thoughtful comments, and Michael had provocative questions. I start with a 20 minute presentation, with slides, so this is the most compact "what is the fiscal theory" video to date. It's at the AEI event page or Youtube

This is another post from an Economic Policy Working Group meeting at Hoover, in which simple undergraduate supply and demand analysis, creatively applied, leads to a surprising result.

Casey Mulligan presented "Prices and Policies in Opioid Markets." Paper, slides and video of the presentation. (Updated link now works)

Once prescription opioids became an evident crisis, the government took steps to restrict the supply, raising the price. Yet opioid consumption and overdoses went up. Explain that Mr. Chicago economist!

Here's the clever answer:

"In the earlier years, opioid subsidies are created and expanded for patients and prescribers while regulations are relaxed. In about 2010 policies begin to swing in the other direction as the with reformulation (see below) and programs discouraging prescription supply to secondary markets. ... enforcement of illicit-drug prohibitions was less of a priority between 2013 and 2016.

(i) heroin was significantly more expensive per MGE than Rx opioids in the 1990s, (ii) illicit opioids became cheaper over time, especially since 2013, and ultimately cheaper than Rx opioids, and (iii) beginning in about 2011, Rx opioids became more expensive or difficult to access for nonmedical use due to regulatory and fiscal changes.

The tide of needle litter came in heavy at the start of every month, when benefit checks arrived and people were briefly flush. .... There were far fewer by month’s end, but when the first of the month came again, a fresh swell always followed.

Michael Shellenberger thought to ask the question, receiving a different and even more uncomfortable answer, theft, though also benefits here.

Don't jump from these observations to a policy conclusion, which is not my point. I don't have an easy solution to the combination of drugs and homelessness. But following the money is surely a question that needs to be asked if we wish to understand the forces behind widespread addiction, and the externalities that drug users create. This might be a case in which paternalism is justified, and cash benefits not such a good idea.

Meanwhile, drug use is apparently way down in Afghanistan, by methods that we would not want to use, but an interesting fact (and an absorbing report) as well.

On Wednesday, Erik Hurst presented a lovely paper, "The Distributional Impact of the Minimum Wage in the Short and Long Run," written with Elena Pastorino, Patrick Kehoe, and Thomas Winberry, at the Hoover Economic Policy Working Group seminar. Video (a great presentation) and slides here.

This is a beautiful and detailed model, which won't try to summarize here. I write to pass on one central graph and insight.

Suppose there is some "monopsony power," at the individual firm level. Don't argue about that yet. Erik and coauthors put it in, so that there is a hope that minimum wages can do some good, and it is the central argument made by minimum wage proponents. In the paper it comes because people are uniquely suited to a particular job for personal reasons. Professors don't like to move, they've figured out the ropes at their current university, so the dean can get away with paying less than they could get elsewhere. Why this applies to MacDonalds relative to the Taco Bell next door is a good question, but again, the point is to analyze it not to argue about it.

"Labor demand" here is the marginal product of labor. (\(f'(N)\) It's what labor demand would be in a competitive market. The monopsnists' demand is lower). Monopsony means that the "marginal cost of labor" rises with the number of employees. There is a core of people that really love the job that you can hire at low cost. As you expand, though, you have to hire people who aren't that attached to this particular job, so you have to pay more. And you have to pay everyone else more too, (by reasonable assumption -- no individually negotiated wages), so the average cost of labor rises.

Thus, the monopsonies firm chooses to hire fewer people \(N_m\), produce less, and pay them a wage \(W_n\) below their marginal product. ("Average cost of labor" is really the labor supply curve, call it \(w=L(N)\). Then \(\max (f(N)-wN\) s.t. \(w=L(N)\) yields \(f'(N)=w+NL'(N)\). The "marginal cost of labor" in the graph is this latter quantity: the wage you pay the last worker, plus all workers times the extra wage you must pay them all. Disclaimer: the equations are me reverse-engineering the graph.)

Now, add a minimum wage. As the minimum wage rises above \(W_m\), we initially see a rise in the number of workers, and their incomes. The firm moves along the arrow as shown. (\(\max f(N)-wN\) s.t. \( w \ge L(N)\), \( w \ge w^\ast\) gives \(w^\ast = L(N)\) .)

Keep raising the minimum wage, though. Once we get past the point that labor supply ("average cost of labor") requires a wage greater than the marginal product of labor, the firm turns around and hires fewer people:

(Really, the problem all along was \(\max_{w,N} f(N)-wN\) s.t. \( w \ge L(N)\), \( w \ge w^\ast\). Once the minimum wage rises enough, the solution \(w^\ast=L(N) \) has \(f'(N)<w^\ast\). The firm does better by hiring fewer people than are willing to work at that wage. With the second constraint slack, \(f'(N)=w^\ast\) is the optimum.)

So, in this best case, minimum wages do first raise employment, and income. But if you keep going, they eventually turn around and lower employment and raise unemployment (people between the equilibrium and the "average cost of labor" curve want jobs but can't get them.) We join the local "monopsony" view with the latter "neoclassical" view.

The actual model is way more realistic, with multiple kinds of workers, firms that can substitute between workers, dynamics that include capital investment in worker-specific technologies, a search model for unemployment and more. Each seems to me just complicated enough to capture an important effect. Multiple kinds of workers is really important: a big part of the "labor demand" is not just a fixed marginal product of a given kind of worker, but the firm's ability to substitute other kinds of workers and machines for a given task. It's nicely calibrated to match the US economy.

A bottom line:

Bit by bit the minimum wage starts to help each group as it hits the point between what they are actually paid and their marginal product.

People whose marginal products are less than $7.50 an hour are missing from the picture. They were already driven out of the market by the current minimum wage. (The conclusions about the optimum minimum wage are potentially flawed by this omission. It could be even less!)

This is a lovely story. An obvious implication: Don't quickly generalize too far from local estimates or small interventions. Big minimum wage changes can have the opposite effects as small ones!

The big question of minimum wages is always which workers are helped vs hurt, not overall labor. Much of the other work on minimum wages (Jeff Clemens, for example) emphasizes that it helps a few, who can work the hours employers want, are already skilled, speak English, etc., at the cost of many others, who tend to be less well off to start.

The dynamic part of the paper is great too. Minimum wages are like rent controls: the damage takes time to show up. In the model, dynamics show up as firms have structured their capital to the current employment mix. It takes time to put in, say, video screens to substitute away from order-takers.

The shaded part is the duration of typical studies. Studies that examine the short run reactions to small minimum wage changes completely miss the long-run effect of large changes.

Finally, once again, the minimum wage like so many other policies, is an answer in search of a question. If the issue is "how does policy address labor market monopsony," the minimum wage is a very ineffective answer to that question. Once you spell out the nature of the actual problem, all sorts of other policies are more effective. If you fix the monopsony, wage subsidies are better. But starting with figuring out why there is monopsony in the first place and what policies are inadvertently supporting it is better still.

****

Update: "Minimum Wages, Efficiency and Welfare" by David Berger, Kyle Herkenhoff and Simon Mongey is a similar paper along these lines -- careful modeling of minimum wages with heterogeneity of workers and firms.

This paper adds different kinds of firms: From Simon:

"when you start accounting for firms also being heterogeneous... a similar logic carries over. A small minimum wage lifts employment at the small firm with a slither of monopsony power before tanking them, while it's tanking them it starts raising employment at the slightly bigger firm, then tanks that. By the time you get up to the wages paid by any firm that might have considerable market power you've blown up employment at a whole load of firms. A perturbation argument essentially leads you to never increase the minimum wage."

Put another way, a minimum wage increase from $7.50 to $9.00 might actually increase employment at McDonalds... because it puts all the taco stands out of business. Then at $12.00, McDonalds goes out of business but Applebees expands, and so forth. (Or, "corner store" and "supermarket" in Simon's beautiful slides with lots of great supply and demand graphs.)

They find that the efficiency maximizing minimum wage is close to where we are now. "Efficiency" means "offsetting monopsony." As in Hurst et al, only a small sliver of people are actually hurt by monopsony and helped by the minimum wage. Everyone whose productivity is below $7.50 an hour is already out of the labor force, and everyone whose productivity is higher than the proposed minimum wage is largely unaffected: